CD Strategies: How To Use CDs To Boost Savings

How and when you invest in CDs can lead to different outcomes. From varying term lengths to investing at different times, we’ll show you CD strategies you can use to boost your savings.

Editor's Note: In early 2024, the yield curve for CDs is inverted: Short-term CDs are paying higher interest rates than long-term CDs. Historically, it has been more common for long-term CDs to pay more than short-term CDs. Most CD strategies assume a normal yield curve, so some of the following strategies may earn less until the inversion ends. Be sure to check current rates and consider your savings goals before deciding if CDs are worth it for you right now.

A ladder, a barbell and a bullet? We aren't talking about a new workout. These are three CD investment strategies you can use that — depending on your situation and goals — might help increase your savings.

If you have some extra money to save and don't need access to it right away, a certificate of deposit could be a good option. By combining CDs at different intervals and times, you might increase your earnings and have money available when you need it.

Here are a few key features of three common CD strategies:

| CD Ladder | CD Barbell | CD Bullet | |

|---|---|---|---|

| Investment Amounts |

Equal

|

Equal

|

Equal

|

| How Many Terms? |

Multiple terms

|

Only two

|

Multiple terms

|

| When Do CDs Mature? |

Every month or year

|

One CD matures soon, while another matures in many months or years

|

All CDs mature at the same time

|

| Best If You Want To |

Maintain revolving access to CD funds without penalties

|

Save for two goals that require short-term and long-term savings

|

Save over time for one significant expense many years away

|

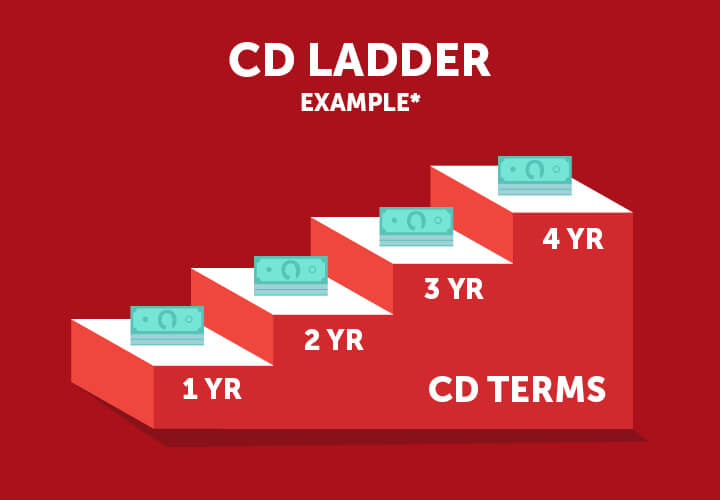

1. CD Ladder Strategy

A CD ladder is a method of dividing up the money you want to invest across CDs, ensuring you always have a maturity date coming up. Open your CDs at the same time with progressively longer term lengths. Your CDs then mature at regular intervals, like climbing the rungs of a ladder.

In a normal CD environment, long-term CD rates (five-year CDs) are higher than short-term CD rates (say, one-year CDs). But you might not want to lock up all of your savings in one five-year CD. It's a long time to wait if you need funds.

With a CD ladder, as one CD rung matures, you can choose whether to reinvest the CD's funds into a new CD. Or move the money into your checking or savings account. A CD ladder ensures you always have a maturity date coming up and can help you avoid "breaking" a CD.

CD Ladder Example*

If you have $10,000, you could put $2,000 each in five separate CDs:

- $2,000 in a one-year CD.

- $2,000 in a two-year CD.

- $2,000 in a three-year CD.

- $2,000 in a four-year CD.

- $2,000 in a five-year CD.

Your CDs will mature every year for the next five years. When your one-year CD matures, you can reinvest in another five-year CD to keep the ladder going, or you can deposit the funds into your checking or savings account for spending.

You'll maximize your return by reinvesting $2,000 plus interest after each CD matures.

You can use CD laddering with many specialty CDs, but using a CD ladder is more common with traditional CDs.

CD Ladder Pros

- You can access some cash once a year on a dependable cadence.

- All of your money isn't locked up in one long-term CD, possibly helping you avoid early withdrawal penalties.

- If rates go up, you can get a higher rate when you open your next CD.

CD Ladder Cons

- If long-term rates are low or dropping, you'll need to research alternatives for your money as the CDs in your ladder mature. Putting your funds into a low-rate five-year CD may be the worst of all worlds because it locks up your funds for a long time at a low rate.

- Challenging to maintain: You'll need to note when each CD matures to either close it or roll it over into a new CD term.

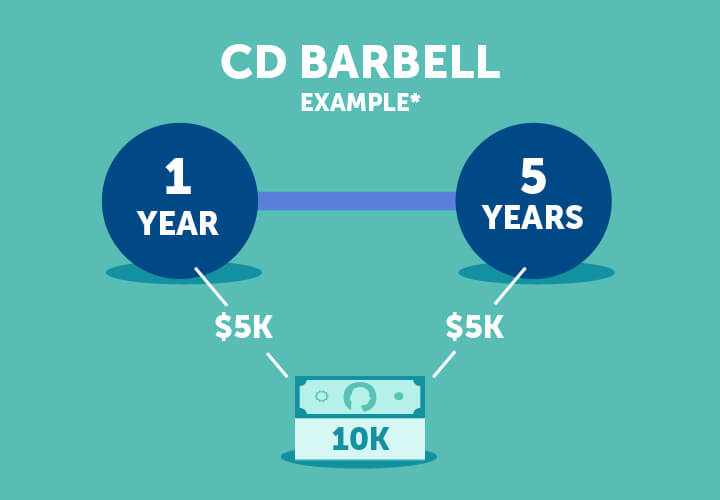

2. CD Barbell Strategy

The CD barbell strategy involves investing equally in two CDs: One short-term CD and one long-term CD. This way, you can earn interest on your money without locking up all your cash in the long term.

CD Barbell Example*

You have $10,000 to save. You put $5,000 in a one-year CD and $5,000 in a five-year CD. Your first CD matures in one year. You can either spend the $5,000 plus interest on your savings goal or reinvest it in another CD.

Meanwhile, the $5,000 in the five-year CD continues to grow over five years.

As a twist on the CD barbell, you could have an uneven barbell, where you put more into one CD than another.

For example, if rates are going down, consider putting more of the $10,000 into the longest-term, highest-rate CD you can find. If rates are going up, you might put more into the short-term CD, knowing you'll be able to pull the funds and put it into a higher-rate CD in the future.

CD Barbell Pros

- A CD barbell helps you save for different goals at different times, such as a car down payment next year and a house down payment five years from now.

- You'll have fewer CD accounts to manage.

- You can shift your savings based on whether you think CD rates will rise or fall.

CD Barbell Cons

- Splitting up your cash this way will result in less compounded interest for the five-year purchase.

- Committing half or more of your savings to a five-year CD makes sense only if the interest rate is higher than you'd find in a savings or money market account.

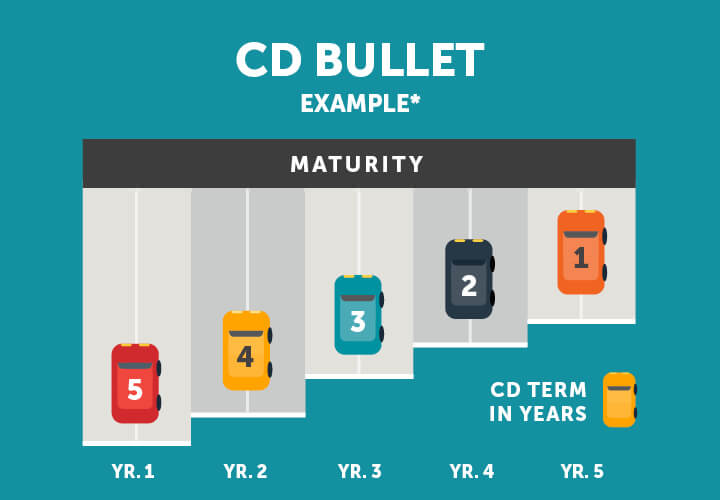

3. CD Bullet Strategy

With the CD bullet strategy, you open a new CD every year, each with progressively shorter terms. So they all mature at once.

CD Bullet Example*

You put $2,000 a year into CDs for the next five years.

- In year one, you put $2,000 into a five-year CD.

- In year two, you put $2,000 into a four-year CD.

- In year three, you put $2,000 into a three-year CD.

- In year four, you put $2,000 into a two-year CD.

- In year five, you put $2,000 into a one-year CD.

All five CDs will mature at the same time. You'll get back $10,000 plus interest earned on all CDs. If you want to collect all your funds together, make sure you open your CDs in the same month each year (say, January).

CD Bullet Pros

- Good if you don't have $10,000 to lock up in savings right now but want to save a little bit every year.

- Can help with financial discipline to commit a certain annual savings amount for a specific goal.

- If rates go up, you could earn more in later years.

CD Bullet Cons

- If CD rates drop significantly over five years, you may not earn much on your later CD deposits.

- Requires discipline to save the money for the next CD deposit date and avoid spending your funds.

Additional Strategies

Think about these strategies in addition to the ones outlined above.

Consider Early Withdrawal Penalties

While you typically don't want to pay an early withdrawal penalty on an existing CD, in some cases, it might make sense if a much higher interest rate is available. Higher interest earned can outstrip a few months of penalty interest.

Don't break your current CD before doing your homework. Calculate the early withdrawal penalty you'll pay against the higher earnings you'll get from moving your money. Review the CD disclosures and run the numbers using online CD calculators to weigh the options.

Investigate Other CD Types

If you've only invested in traditional CDs, research new CD options. For example, no-penalty CDs won't hurt your returns if you withdraw funds before maturity. (BECU doesn't offer this type of CD). A bump-up CD can help you manage interest rate fluctuations and ensure you won't miss out on a rate increase. An add-to CD allows you to deposit more money in your account after opening it.

Combine CDs with Other Accounts

If interest rates fluctuate, you can divide your emergency savings into different goal buckets. You could think about putting one month of living expenses into a traditional savings or high-yield savings account, also called HYSA, for immediate access. Then, you might put other funds you want to leave untouched into a CD. (BECU doesn't offer HYSAs).

FAQs About CD Strategies

Is a CD Ladder a Good Idea in 2024?

CD ladders and other strategies often assume increasing or higher longer-term rates, said Scott Smith, head of BECU's deposit product strategy with 22 years of service in the credit union industry. When CD rates revert to a more normal, predictable yield curve, it may be better timing to use a CD strategy such as a ladder, barbell or bullet.

Should I Invest in a CD or Pay Down My Credit Card?

Interest charged by a credit card will outweigh any returns you'd earn from a CD. Build your liquid emergency fund and pay down high-interest debt before prioritizing your CD.

What is the Best CD Strategy Right Now?

The best CD strategy right now may be to open a shorter-term CD while interest rates are still on the higher side, Smith suggested. If CD rates drop, you may not be able to get the same rate you can in early 2024. If rates are the highest they'll be in a while, seek out the longest-term CD at the highest rate.

The Big Picture

CDs can be one more way to help you save money for future needs or a big purchase. CDs offer a stable return without the unpredictability of the stock market. However, you may lose some of your returns to penalties if you withdraw money from your CD early. Compare these strategies to take advantage of today's favorable rates without risking your returns.

* Where examples are used, the products, rates and returns are not guaranteed and are for educational purposes only. The information and examples are not advice and may not reflect the rates, products, or services currently available from BECU. BECU does not offer or guarantee products or rates in this article.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized financial, tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation when making financial, legal, tax, investment, or any other business and professional decisions that affect you and/or your business.

Related Content

Lora Shinn

Contributor